{kind=link}

As another tax filing season comes to a close, millions of Americans have reduced their taxable income through accounts that help pay for medical costs. Under current law, people can make limited pre-tax contributions to and withdrawals from a “health savings account” (HSA), or let the money appreciate in value on a tax-free basis. In addition to being a frequent flyer in Republican health plans, including the recent Republican Study Committee budget proposal, members of Congress have put forth bipartisan proposals to expand HSAs. But with the benefits of HSAs primarily accruing to healthier and wealthier Americans, expanding HSAs could exacerbate an already regressive tax break without improving access to coverage or care.*

Background

HSAs are an account permitting individuals to save money on a pre-tax basis that can fund certain qualifying medical expenses. Accounts offer a “triple” tax break—contributions, investment growth, and withdrawals for eligible expenses are all exempt from federal taxation. Annual contributions are capped—in 2024, individuals age 55 and under can contribute up to $4,150 for self-only coverage or $8,300 for family coverage. Limits for those over 55 are higher. Employers can also contribute to workers’ HSAs.

HSA holders are required to pair the account with a high-deductible health plan (HDHP). To qualify as an HDHP in 2024, a health plan must have a deductible of at least $1,600 for self-only coverage and $3,200 for a family plan. In 2023, workers with HSA-qualifying HDHPs had average annual deductibles of $2,518 for self-only coverage.

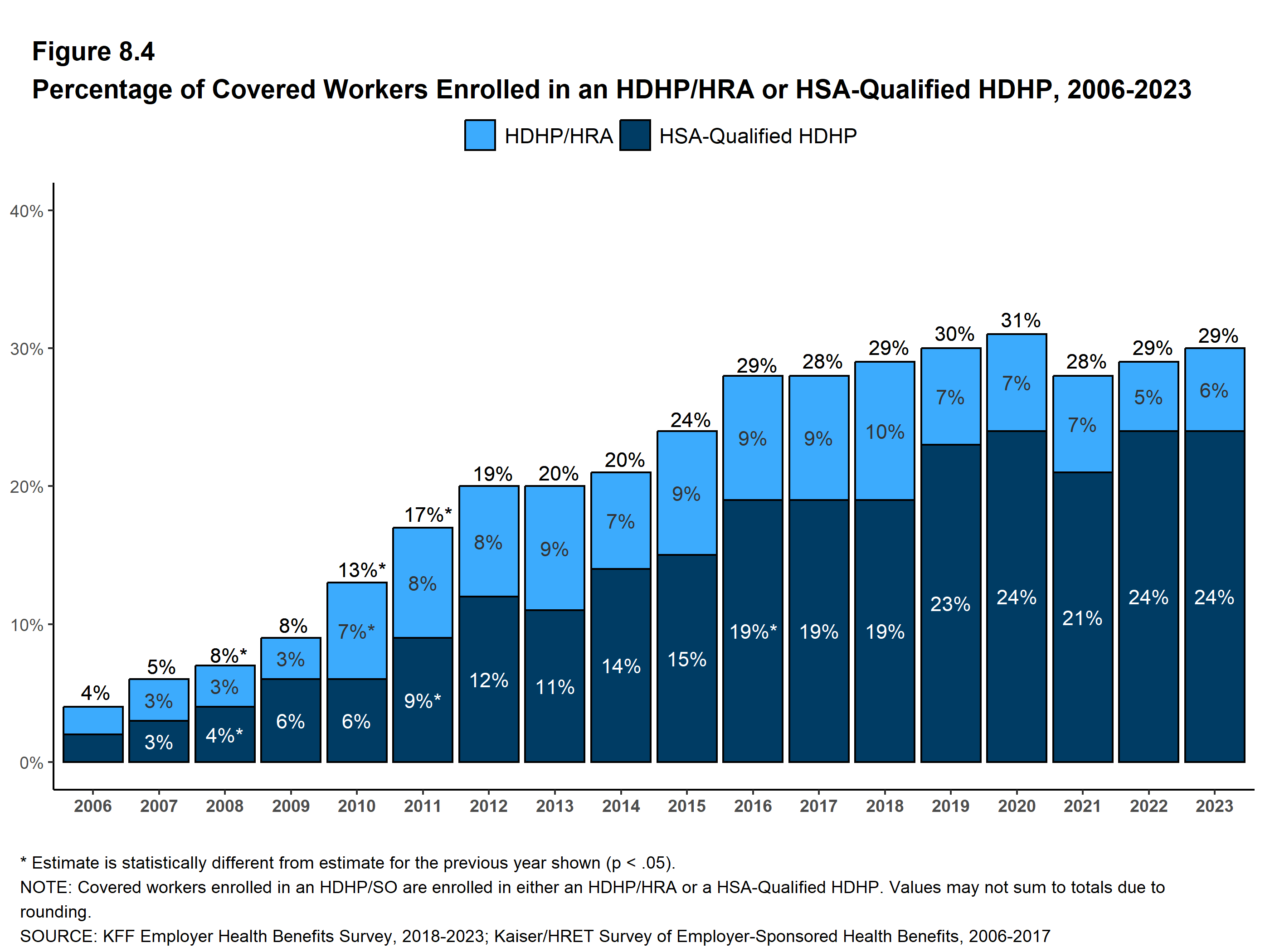

As of 2021, around one in six adults with private health insurance had an account, and in 2023, nearly one in four workers with employer-sponsored health insurance enrolled in an HSA-qualified HDHP (up from around one in 10 covered workers in 2013).

{kind=link}

In theory, this arrangement gives enrollees “skin in the game,” encouraging them to shop around for lower health care prices and deterring utilization of low-value or unnecessary care. This dynamic is supposed to reduce health spending and promote an efficient health care system. But embedded in the HDHP-HSA arrangement is a regressive tax break and penalty for poor health that creates barriers to care for people who need it most.

The Evidence is Clear: HSAs Help the Healthy and Wealthy at the Expense of the Sick and Poor

Income Disparities: A Tax Subsidy That Primarily Benefits Wealthier Individuals

Most of the uninsured are in a lower income bracket, but HSAs disproportionately benefit the wealthy. HSAs provide the greatest subsidy to people who need it the least; tax-free contributions are most valuable to people in the highest tax brackets and least valuable to lower income individuals. Unsurprisingly, high-income households are more likely to make HSA contributions or receive contributions from their employer, and tend to contribute more money to HSAs than lower income account holders.

These income disparities are further exacerbated by the role HSAs serve as a tax shelter and investment vehicle. HSA contributions decrease taxable income, and account holders can withdraw funds as reimbursement for previous medical expenses without increasing their taxable income, which could, for example, allow them to avoid entering a higher tax bracket. The accounts have also been touted as a tax-free investment option—an especially attractive one for people who have already maximized contributions to other tax-advantaged accounts like an IRA.

Health Disparities: Helping the Healthy and Penalizing the Sick

In addition to income disparities, HSAs exacerbate health disparities by increasing costs for sick people while reducing costs for healthier individuals. Account holders are required to enroll in HDHPs, less generous health plans with higher out-of-pocket costs. While these plans often come with lower premiums than products with lower deductibles, they can ultimately be more expensive for people with chronic conditions or other health care needs. HDHPs are a much better deal for healthier individuals who use less care.

Accordingly, HDHPs paired with HSAs tend to be more attractive to the healthy and wealthy. Using the combined tax break and lower premiums associated with HDHPs, HSA holders with substantial contributions and few health care needs may put account funds towards things like gym memberships and meal kits, testing the limits of what qualifies as a medical expense under current guidelines.

Barriers to Care for Low-Income Enrollees

Consumers who cannot afford to sufficiently fund HSAs may face barriers to care. HDHPs impose high cost sharing, a blunt instrument known to reduce utilization of both effective care and ineffective care. These plans also cover fewer pre-deductible services—HDHPs can only cover preventive care pre-deductible (including a limited set of services prescribed to treat individuals with certain chronic conditions), subjecting enrollees to the full cost of many items and services until their high deductible is met.

Because of these cost barriers, enrollment in HDHPs is associated with delayed and foregone care, particularly among people with lower incomes. Even use of preventive care—which must be covered without cost-sharing by HDHPs—is lower among HDHP enrollees, due at least in part to enrollees’ lack of awareness of free care and potentially concerns about the cost of follow-up care.

Lower income HDHP enrollees who end up needing health services may face additional obstacles; episodes of care can leave them with big bills, and private insurance enrollees with high deductibles are at a greater risk of accruing medical debt.

This Regressive Tax Shelter Does Not Reduce HSA Holders’ Health Spending

The primary beneficiaries of HSAs may not be bending the health care cost curve as intended. Recent evidence suggests that people enrolled in HDHPs with HSAs are not using less care compared to their counterparts who don’t hold an HSA, and HDHP-HSA enrollees are reporting fewer financial barriers to care than in the past. Researchers have suggested that, as cost sharing increases across private plans, higher-income Americans receiving the additional “subsidy” from HSA tax benefits may be using it to obtain more care.

Congressional Proposals to Expand HSAs Would Exacerbate These Issues

The current Congress has considered several bills to expand HSAs, including:

- Giving Employers a Pass on the Requirement to Offer Health Insurance: another proposal wouldallow large employers to satisfy the Affordable Care Act’s “employer mandate” by funding HSAs for employees to purchase a Marketplace plan, relieving them of their current duty to offer coverage.

These proposals would predominantly help higher-income and healthier individuals, who benefit more from the tax advantages of HSAs and already face far fewer barriers to coverage and care, by making HSAs more lucrative and flexible. Expanding HSAs would also further incentivize healthier and wealthier individuals to purchase less comprehensive coverage, exacerbating the existing dynamic that rewards individuals with fewer health care needs and penalizes the sick.

Money Subsidizing Wealthy Enrollees Could Instead Fund a Major Coverage Expansion or Affordability Initiative

HSAs divert federal funds away from more effective coverage expansions. The tax benefits of HSAs reduce federally taxable income and consequently federal revenue. Treasury estimates that tax exclusions for HSAs (and a similar medical savings account that preceded HSAs) will cost the federal government nearly $180 billion over the next ten years. On top of this cost, two bills marked up last year by the House Ways and Means Committee, including proposed bipartisan legislation, are expected to reduce revenue by an additional $71 billion between 2024 and 2033 if enacted.

Federal expenditures associated with HSAs and proposed expansions could instead fund efforts to reduce the uninsured and improve health insurance affordability. The Center on Budget and Policy Priorities has pointed out that, over the next ten years, the estimated cost of closing the Medicaid gap is $200 billion, while permanently extending the temporary Marketplace subsidy expansion under the American Rescue Plan Act, which helped produce record Marketplace enrollment, would cost $183 billion.

Takeaway

Access to affordable, comprehensive insurance is still not a reality for all Americans. An ongoing issue to achieving universally affordable coverage is the underlying and rising cost of care. Unfortunately, experience suggests that expanding HSAs will not tackle this problem or meaningfully expand coverage. The loss of federal revenue associated with HSAs’ regressive tax cuts could thwart policies that expand health care access for people with the greatest need—those who are currently least likely to have access to affordable coverage and care.

*Author’s note: this blog was updated on April 16, 2024 to add information about the share of people with private insurance who have HSAs and to add clarifying language concerning the revenue impact of proposed federal legislation.